How to Save Money on Maternity Leave: Practical Tips for New Parents

Updated January 15, 2026

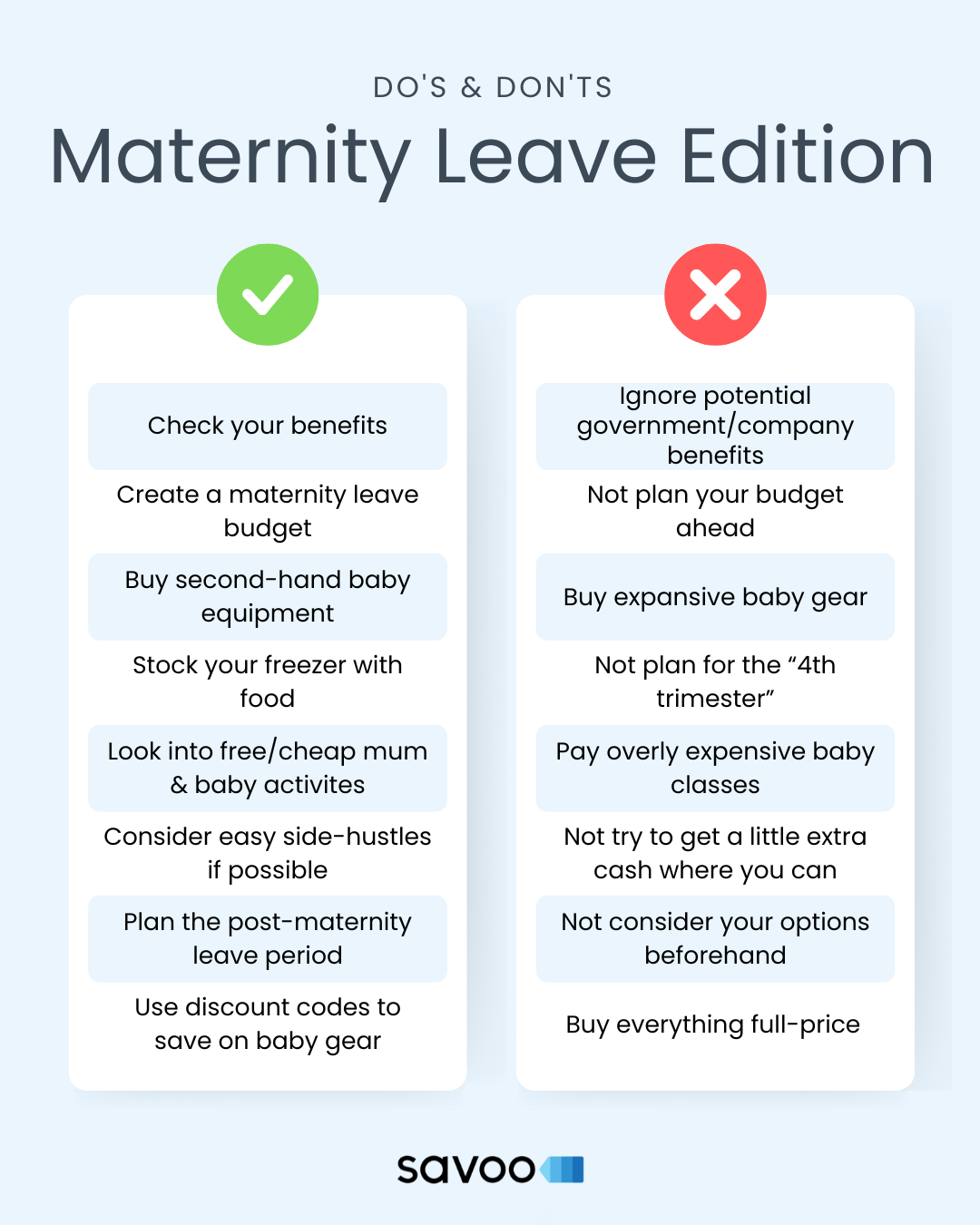

Key Takeaways

- Plan early to reduce financial shock: Use the months before leave to trim subscriptions, start a dedicated savings buffer, and build a realistic maternity budget so reduced income is easier to manage.

- Know which benefits apply to you: Use the months before leave to trim subscriptions, start a dedicated savings buffer, and build a realistic maternity budget so reduced income is easier to manage.

- Prioritise baby essentials and low-cost options: Accept safe second-hand items, use seasonal sales and voucher codes, and create a registry to avoid duplicate purchases and expensive impulse buys.

- Plan your post-leave pathway now: Decide whether you will return full-time, part-time, or take a longer break, and model the financial consequences of childcare, reduced hours, or a single income.

Maternity leave is not exactly a relaxing break from work. It is a special time to bond with your baby and adjust to life as a parent, but stepping away from work for several months can put real pressure on your finances, even with maternity pay and benefits in place. Add in the cost of essentials like a cot, car seat, and pushchair, and it is easy to see why money worries can creep in alongside the sleepless nights.

The good news is that there are practical ways to reduce that financial strain. This guide explains how to save money on maternity leave, so you can spend less time worrying about your bank balance and more time focusing on your new family member.

Plan for your maternity leave ahead of time

Most people get a decent heads-up when it comes to maternity leave. That gives you around eight months to plan for the drop in income and make adjustments gradually.

Start saving as early as you can and look closely at your regular outgoings. Review monthly bills and subscriptions and cut anything you do not really use. For example, do you need multiple streaming services, or could you make changes to your food shopping to reduce your weekly spend? Check out our “How to save money" article to know more about budgeting and download our free budget planner.

Making small changes early often feels easier than trying to cut back once your baby arrives.

Getting your head around your benefits

Understanding what financial support you are entitled to can make a big difference. Eligibility and payment amounts depend on your circumstances, but the following are the main options for most parents in the U.K..

| Benefit | Who can claim | 2026 rates | Notes |

|---|---|---|---|

| Statutory Maternity Pay | Anyone employed, earning £123+ per week, with 26+ weeks’ service | 6 weeks at 90% pay, then £187.18/week or 90% of avg. week’s pay (whichever is lower) for 33 weeks | The final 13 weeks are unpaid unless the employer enhances |

| Shared Parental Leave & Pay | All birth or adoptive parents meeting all criteria | £187.18/week or 90% of your avg. week's pay (whichever is lower) | You can share up to 50 weeks of leave and 37 weeks of pay between both parents |

| Child Benefit | All parents of children under 16 | £26.05 eldest/only child, £17.25 additional child (weekly) | Higher earners may repay via tax |

| Universal Credit | Low household income, savings under £16,000 | Between £316.98 and £628.10 depending on situation | Extra amount possible for households with children |

Figures are provided for guidance and were current in January 2026. Always confirm the latest rates and eligibility on official sources such as gov.uk.

Combined, these benefits can help soften the impact of reduced income during maternity leave.

Create a maternity leave budget

Once you know roughly how much you will receive from maternity pay and benefits, you can build a realistic maternity leave budget. Here is your maternity budget checklist:

- Total household income during leave

- Rent or morgage

- Utilities and council tax

- Food and essentials

- Transport and travel

- Child-related costs

- Debt repayments

- Emergency savings

Seeing everything clearly laid out can help you spot areas where you can cut back and make the whole process feel more manageable.

We spoke to Alison Green, director at WOMBA (Work, Me and the Baby), who shared her advice on managing money around maternity leave:

We often hear working parents thinking about their incomes individually and perhaps reaching the conclusion that it's not worth one of them (often the mum) working due to the high costs of childcare. Thinking about household income and taking a medium-term as well as short-term view can be a good basis for decision-making for the family as a whole and the careers of both parents. With this in mind, before maternity leave, try to review your finances jointly. Having a baby will change the way you deal with joint decisions around household budgeting. So as a couple, set aside some quality, uninterrupted time to talk frankly about money and get into the habit of doing this regularly.

Focus on baby-related expenses

Baby essentials add up quickly, especially for first-time parents. Items like a cot, pushchair, car seat, high chair, clothes, and nappies can take a large chunk out of your budget.

If friends or family have children, consider accepting hand-me-downs. Many baby items are used for a short time and can be just as safe and practical second-hand, as long as they meet current safety standards.

My colleague Céline Pastezeur, who recently welcomed her second child, advises:

From experience, it’s best to get to know your baby before investing in fancy and expensive equipment such as a bouncer or a carrier. We tend to buy these items thinking they’ll make our life easier, but the truth is: not all babies love them! We had to buy two different bouncers for our firstborn before finding “the one". And in the end, we sold it because our second child hated being seated that way!

When you do need to buy new items, timing and discounts can help. Seasonal sales, retailer promotions, and voucher codes can all reduce costs. Savoo lists current voucher codes for retailers such as Boots, Argos, and Smyths Toys, as well as savings on baby clothes, maternity items, and car seats and prams.

To save further on baby apparel or equipment, Céline also recommends buying and selling second-hand:

Let’s be real: babies grow fast! Even if it’s tempting to buy them shiny new clothes, odds are they’ll only wear them for a few weeks before outgrowing them (or staining them forever, if you know, you know…). So if you want to save a few precious pounds, hit second-hand websites like Vinted or eBay. You can also sell all the items that your little one no longer fits into to make some money back.

You may also want to create a baby registry. Friends and family often like to help, and a clear list of essentials can avoid duplicate or unnecessary gifts.

Look for free mum & baby activities

Research your local Children and Family Centre to access a wide range of free activities and resources to support both you and your baby. From children-specific activities, like learn and play sessions and post-natal courses, to wider skill development sessions, like debt and money management or healthy eating, you’ll find a lot of ways to feel supported and connect with your community.

My colleague Céline explains:

While on maternity leave, I took part in a three-week course to learn how to massage my baby. We also attended weekly baby sensory play and music sessions, where coffee and biscuits were sometimes provided for the mums (and fruits for the babies). Another activity I really appreciated was free stretching sessions for mums and babies, led by a mental health professional who created a safe space for mothers to take care of themselves physically and mentally. All of these activities were wonderful opportunities to bond with my son and connect with other mums, and they were completely free thanks to my local council.

Try to avoid getting into additional debt

It is best to avoid using credit for non-essential spending during maternity leave. Credit cards and loans can quickly become expensive once interest is added, especially when your monthly income is lower.

If you already have debts, it may be worth exploring ways to reduce interest, such as consolidating balances or using an interest-free credit card if appropriate. Make sure all repayments are included in your maternity leave budget to avoid surprises. Check our “How to become debt-free" blog to learn more about debt management.

Consider work from home opportunities

Looking after a baby is demanding, but there may be occasional windows of time when you can earn a little extra, if you want to, and it feels manageable.

Options might include freelance work, tutoring, or other flexible online tasks that fit around your existing skills. You can register on platforms like Fivrr and use your skill-set to earn a bit of money, whether it’s through programming, writing, tutoring, or even just peer support. Other options include answering surveys online. Some websites will have you answer a few questions if you fit the demographics of their study, and you can earn some cash or gift cards in exchange.

Be realistic about what you can take on and avoid overcommitting, as rest and recovery are just as important.

Plan for what happens after maternity leave

Deciding what to do when maternity leave ends can feel daunting, especially while you are still adjusting to life with a baby. Thinking through the main options early can help you avoid rushed decisions and unexpected costs.

Most parents fall into one of three paths. Each comes with different financial considerations.

Option 1: Return to work full-time

If you plan to return to your previous role or hours, childcare is usually the biggest new expense to plan for.

Key things to consider:

- Childcare costs, including nurseries, childminders, or nannies.

- Commuting costs if you are travelling to work and to your childcare service.

- Changes to benefits, such as Universal Credit or help with childcare costs.

- Whether your employer offers flexible working or salary sacrifice schemes.

It can help to compare your take-home pay after childcare costs with your current maternity leave income, rather than looking at salary alone.

Option 2: Return to work part-time or flexibly

Reducing your hours or working flexibly can make childcare more manageable, but it also affects household income.

Key things to consider:

- Reduced earnings and how this impacts your monthly budget.

- Whether you still qualify for certain benefits or childcare support.

- How flexible working arrangements may affect career progression.

- The balance between paid childcare and informal support from family or friends.

Running a revised budget based on your new hours can help you see whether this option is sustainable in the short and medium term.

Option 3: Leave employment or take an extended break

Some parents choose not to return to work straight away. This can reduce childcare costs, but it usually means relying on a single income or savings (although options are available through Shared Parental Leave and Pay.

Key things to consider:

- Living on one (full) income and adjusting long-term spending habits.

- Eligibility for benefits and support when one parent is not working.

- Pension contributions and long-term financial planning.

- How and when you might return to work in the future.

If this is your plan, updating your household budget well in advance can help you avoid financial shocks later on.

Save money on baby purchases with voucher codes from Savoo

With less money coming in, knowing how to save during maternity leave can make everyday life feel more manageable. Small savings on regular purchases can add up over time.

Savoo offers a wide range of up-to-date voucher codes to help reduce the cost of baby essentials and household spending. Browse Savoo voucher codes to find ways to make your maternity pay stretch further.

You May Also Like

Comprehensive Back to School Checklist

by Emily Ambler | 18/8/2025

How to Get Cheap Alton Towers Tickets

by Emily Ambler | 30/7/2025

40+ Places where Kids Eat Free this summer

by Emily Ambler | 16/7/2025